Public activity as measured in hard numbers by ActivistInsight, is down significantly in Q1 2020. However, it is a tenuous metric, especially during times of severe dislocation. The market turmoil caused by COVID-19 creates an abundance of opportunities for activists: valuations have plummeted almost across the board and stark differences between companies´ ability to cope with the crisis are becoming increasingly apparent. Moreover, the pandemic will lead to a reassessment of corporate vulnerabilities, and open new doors for activists. ESG is likely to become one of those new doors, with social (‘S’) aspects gaining importance during the pandemic.

So there is plenty of activity, but behind the scenes and not measurable, for now at least: activists are active, increasing existing positions and preparing for re-engagement with businesses post COVID-19.

At the same time, poison pills are resurfacing, tolerated and sometimes even encouraged by authorities. But as in the past, they will be of limited help if activists´ arguments appeal to other shareholders, and possibly a wider set of stakeholders.

As companies regain bandwidth to look ahead further than a few days, they would do well to analyse their new vulnerabilities. That shareholder activists are a bigger threat than strategic buyers is even more true today than when we published this article in February 2020.

Shareholder activism is very much active

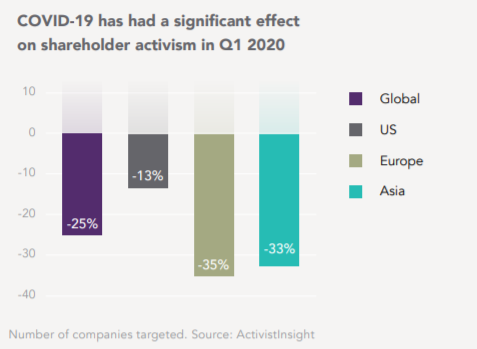

Publicly known activist campaigns in the first quarter of 2020 are down by about one quarter globally on the same period last year, according to ActivistInsight. The downturn was less pronounced in the US (-13%) than in Europe and Asia, which are both down about one-third. This drop becomes even more remarkable taking into account Lazard´s observation in its Q1 2020 report that activism had gone off to a strong start in the first two months of 2020, driven by activity in Europe, with more than $13bn of capital deployed worldwide. The drop-off in activity in March, when the COVID-19 pandemic really started to bite in Europe and the US, was precipitous.

Are shareholder activists in Europe retrenching? Does the COVID-19 pandemic, and the deep economic crisis following on its heels, give companies protection? We do not see it: all the evidence we have collected over the last few weeks, statistical and anecdotal in many conversations with a range of market participants, shows that activists do what they always do; they are active. Christopher Ludwig, Head of Strategic Shareholder Advisory at Credit Suisse, confirms this:

“Many of the largest activists are not suffering redemptions and we have seen them taking positions throughout – value investing is core to their thesis after all. Notably, they are staying under the registration threshold in order to get the benefit of a few months of working with management on friendly terms behind the scenes. We are not seeing the mid and smaller activists as much, and I am assuming that is because many are staying on the sidelines for now as they work through LP redemptions.”

Darren Novak, Head of Activist Defence at UBS, takes a similar view:

“Activists were put on earth to take advantage of dislocations. That is what they do. They are the most opportunistic of opportunistic investors. They are like distressed debt investors in a way – they see the opportunity when no-one else does."

A variety of responses, but no retrenchment

It is true that some activists have decided to take a step back. A fundamental reason for this also surfaced during the financial crisis more than 10 years ago: “Volatility generally is not conducive to activism”, says James Thomlinson, Head of European Activism Defence at Jefferies. “They need a multi-month runway to prepare their campaigns.” But another reason, according to Richard Thomas, Head of European Shareholder Advisory at Lazard, is credibility: “In order to hold sway with managements of target companies, activists´ demands need to be credible with their fellow, non-activist shareholders.” Asking for share buybacks, higher dividend payouts or operational improvements in the context of disappearing revenues and cash flows just does not cut it. Nor do demands to replace management while companies are facing a once-in-a-century crisis. In that sense, activists have “lost some arrows in their quiver for now”, as Thomas puts it.

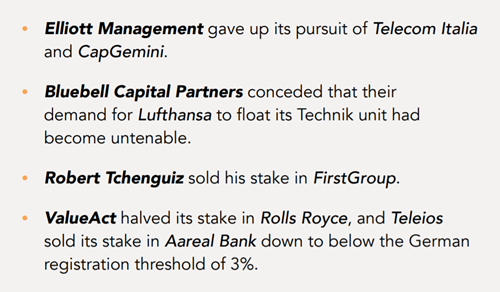

As a result a number of campaigns were put to rest in March:

While reputational considerations seem to have played on some activists´ minds at the very beginning of the pandemic, they abated swiftly: “Reputation is no major concern for shareholder activists, and it feels like we have got back to business quite quickly”, says James Potts, Head of EMEA Activist Defence at Barclays.

In fact, many more activists have taken advantage of the unprecedented market dislocation by ratcheting up pressure and / or opportunistically increasing existing positions at much more attractive valuations than only a few short weeks ago:

What goes around comes around

On balance, therefore, while activists may well be less visible in Europe for now, this seems to be largely tactical. And why would they stay on the sidelines? Even after the recent market recovery, driven almost entirely by extreme fiscal and monetary largesse in an attempt by governments to stave off economic collapse, company valuations remain at least 20% cheaper than only two months ago. Certainly on an assumption of a V-shaped recovery, activists now have much more downside protection for their campaigns.

The outlook is also promising. Tibor Kossa, Co-Head of M&A at Goldman Sachs in Germany, predicts a “bifurcation of fortunes for the corporate sector”. Here, COVID-19 is already creating relative winners and losers. Winners will come out with less impacted balance sheets, ready to drive consolidation or mop up assets from competitors forced to repair theirs by selling businesses. Plenty of opportunity for activists to get involved, either opportunistically or on fundamental grounds. Kossa´s Co-Head Christopher Droege adds: “The dust needs to settle. But over the coming months, we are likely to see a growing number of companies with balance-sheet fire-power looking at acquisitions again.” Looking back at the financial crisis in a recent blog, ActivistInsight supports this view: “While 2008 was quiet, activism came back strongly in the immediate aftermath of the crisis as a stabilizing market left many companies exposed, both in terms of performance and governance.”

The pandemic will lead to a reassessment of corporate vulnerabilities: how has the world changed, and companies strategic positioning in it? Where are the new weaknesses? Are very specialized, very focused business models, or companies with complex supply chains, now outdated? Which companies went into the crisis ill-prepared, with shaky balance sheets? Whose internal processes did not hold up in a world turning on its head, and whose ability to communicate with their employees and external stakeholders? Which managements were not up to the task? Additionally, how will companies have managed their restart as lockdowns came to an end, and how fast will they have been out of the gates relative to competitors?

Finally, some companies may try to use the difficult environment as an excuse to defer tough decisions or ignore governance weaknesses – another entry point for activists.

The ´S´ – moving up in the ESG family hierarchy

There was a suggestion early in the pandemic that ESG would have to take a back seat while companies fought for survival and the global economy reeled from a severe recession. Two months into the crisis, there are strong indications that this will not be the case. Especially the ´S´, long something of an orphan in the ESG family, is quickly turning into its matriarch. How companies have dealt with their employees first and foremost, but also with their suppliers, landlords and customers, is unlikely to be forgotten after the crisis. Look at Sports Direct in the UK or Adidas in Germany. James Thomlinson from Jefferies again: “The way corporates have acted through the pandemic is going to be front and centre after it, whether examined by an activist or shareholders more generally. There will be a look-back test, definitely. Part of the future resilience assessment, of their licence to operate, will be how companies interacted with their stakeholders, not just shareholders, and especially with their employees. There will be much more scrutiny of corporate responsibility and we are starting to see activists using that as a tool to broaden their campaign and win support.”

As highlighted in our recently published article Corporate Responsibility in a Post-COVID-19 World, businesses that are responding to COVID-19 with strong corporate citizenship and strategically communicating their actions are reaping the benefits.

A number of influential investors have gone on record in support of the ´E´ as well. Anecdotally, many more institutional investors who have not gone public are also paying more attention to ESG issues, not necessarily only because of their own conscience but for fear of their reputation with their sponsors and the general public.

The re-emergence of the poison pill

A trend which may provide some, albeit limited, protection to companies, already in evidence before this crisis, is strengthening: governments around the world are adopting a more defensive stance against foreign M&A, and a more tolerant stance towards corporate poison pills. And companies are taking advantage: according to ActivistInsight Governance, 20 have adopted poison pills so far this year, compared with only 18 in all of 2019 and 15 in 2018. Companies that feel vulnerable to takeover bids and opportunistic buying as a result of plummeting market capitalisations are rushing to raise defences previously frowned upon. For example, Toshiba Machine's AGM approved a poison pill measure, enabling the company to repel an unsolicited takeover offer by City Index Eleventh, a fund backed by activist Murakami.

But let´s remember activists´ playbook: while increasingly, they prefer to approach and settle behind the scenes, they are not shy to go public if a collaborative attitude does not lead to success. And when they do, and their fellow shareholders agree with their arguments, even poison pills offer little protection.

What this means for companies

Unlike the financial crisis 2008, at least the big activist players have plenty of capital, and some of them are raising additional funds even during the depth of the pandemic. Clearly, they are now very focused on their existing portfolios and the damage the pandemic has done to them, but not in the same existential way that they were 12 years ago, when it was a matter of whether they were going to be operating the next day. They are on a much sounder footing today than back then and the pressure to deploy capital has not diminished. There is an expectation in the market that, initially, there will be a lot of below-the-radar value investing by activists in companies that are fundamentally oversold and do not necessarily depend on significant change. “True value-investing, but on steroids”, as one banker put it.

Darren Novak again: “While activists are avoiding aggressive public campaigns for now, they are identifying new names, finalizing due diligence on them and positioning themselves in order to buy into them once we come out of the crisis. We are seeing a fair bit of outreach privately and of course a tremendous amount of chatter privately. Activists are reaching out to new targets, but with a gentler approach. They initially talk to IR rather than the board, trying to gain a better understanding of these businesses."

But a full return to normal operations is on the cards, the crisis is likely to offer plenty of new opportunities to get involved, and initial concerns harboured by some activists around being perceived to be profiteering have abated. The full range of activist entry points will become available again as companies get to grips with the initial impact of the pandemic and fellow shareholders begin to listen again to arguments beyond the immediate survival of companies. Perhaps there will even be new, additional entry points as companies struggle with the challenge of returning to normal operations, and as ESG considerations, newly anchored by the ´S´, gain in relevance and establish themselves. The difficulties caused by continued share price volatility are likely to be outweighed by the downside protection provided through lower company valuations.

As companies regain bandwidth to look ahead further than a few days, they would do well to analyse their new vulnerabilities.

That shareholder activists are a bigger threat than strategic buyers is even more true today than when we published this article in February 2020.